When you’re young, money is easy. Spend less than you earn, save what you can, and don’t take on too much debt.

No problem, right?

But there comes a time in everyone’s life – regardless of your level of wealth – when the complexities of your finances become too intricate for rules of thumb. Saving for retirement, investing, paying for your kids’ college, navigating tax laws, caring for aging parents – at some point, everyone will struggle to make heads or tails of some financial detail or other. Unfortunately, life won’t slow down to give you space to sort it out.

When you reach that point, you have a few options:

- Hire a financial advisor

- Go the DIY route

- Ask your financially savvy uncle for help

- Take advice from influencers on social media (Please DON’T take advice from influencers on social media. I only brought it up so I could warn against it! Social media is jam-packed with people who either don’t know what they’re talking about or have hidden motives behind their advice.)

If you ask us, we like option A (of course). But it’s not the only viable option.

Whichever route you choose, it’s important to be aware of the tradeoffs, the most obvious of which is time and money.

If you choose to do it all yourself without working with an advisor, you get to keep the money you would spend to hire someone, but you give away your time in the form of research and managing investments on your own. If you choose to work with a professional, you get to keep your time, but you give away some money to pay your chosen advisor.

There are other tradeoffs, of course. Personally, I firmly believe that hiring an advisor – a good advisor – is worth it.

Today, I want to talk about eight ways that hiring a financial advisor can improve your life.

1. Less stress of managing finances, for yourself and your spouse

Some of the downsides of managing your own investments are more obvious: hours of research, costly mistakes as you learn, keeping up with the markets every day…

But here’s one of the DIY downsides that people often don’t recognize: Managing your own investments is stressful – for both you and your spouse.

If you’re the one overseeing finances, when something goes wrong you feel like it’s your fault (and your spouse may or may not agree with you ). As a result, you’re constantly checking the markets and second-guessing yourself.

The truth is that no one has ever perfectly navigated the markets. Risk is part and parcel of investing. As an advisor, I navigate the risks of the market and help my clients make sense of gains and losses every day .

When you hire a financial advisor, you offload that stress to a professional who handles these matters for a living and can help you maintain a healthy, long-term perspective.

Related: Why Choose Clarity? Three Quotes from Real Clients on Why They Work with Us

2. Gain clarity around what retirement will look like

Most people go through two phases when it comes to how they think about retirement:

- The first phase is during the first half of your career, when you have a nagging voice in the back of your mind telling you that you should probably save more or create a plan of some sort.

- The second phase comes during the latter half of your career, when retirement becomes an urgent matter that can dominate your thoughts and keep you up at night if you dwell on it too long. Are you ready? Could you do more? Where will you live? When should you claim Social Security?

In other words, retirement can go from “really far away” to “coming up really fast” almost overnight. For that reason, people often struggle to approach it with much clarity.

Financial advisors can help remove the uncertainty and urgency from retirement by:

- Estimating how much you need to save for retirement

- Building a tax-efficient retirement income plan that matches your expenses

- Helping you successfully navigate life transitions like changing careers, receiving an inheritance, losing your spouse, and more, all without losing sight of the retirement picture

No more nagging voice, no more sleepless nights.

3. Spend money now without worrying about how it may impact the future

A lot of people think financial advisors don’t want you to enjoy your money now – they only care about saving and investing as much as you can for retirement.

Nothing could be further from the truth.

One of my favorite things about being an advisor is that I get to help people free up money in the present by finding clarity about the future. When you have a financial plan for tomorrow and you save according to the plan, you have a clear picture of what qualifies as “spending money” and you don’t have to feel guilty using it however you want.

4. You get a lifelong professional decision-making partner who understands your situation deeply

People often think that no one else could care about their financial future as much as they do. Why hire an advisor if they won’t care as much as you do? But if you take that same logic and apply it to your health, why would you ever hire a doctor?

In the same way that a doctor is a lifelong partner in your physical health, a financial advisor is a lifelong partner in your financial health. We do annual check-ins, we’re available for appointments as needed, we provide guidance in financial decision-making, we know your goals, we know your history…

Whether it’s budgeting or figuring out how to minimize your tax burden, we help you make better decisions today so you can be more financially “healthy” in the long term.

Long-term relationships with clients are another of my favorite things about being an advisor: I get to help our clients dream and plan for the life they want, and then cheer them on when it becomes reality.

Related: The Clarity Difference: Learn What Sets Us Apart from Other Financial Advisors

5. Access a shame-free zone to share private details & ask questions you may feel embarrassed to discuss elsewhere

A number of people never ask for help because they’re scared they’ll be judged for making “dumb” decisions or asking “dumb” questions. It’s a far too common predicament, and a dangerous place to be.

When it comes to big decisions like planning for retirement, the consequences of inaction are too great to let insecurity keep you from getting help. Every year you put off getting a financial plan in place, you lose a year of compounding interest and goal-focused saving that could help you get on track.

As financial advisors, we’ve seen it all. From costly decisions to zero savings to huge debt, we’re rarely surprised – and even when we are, we’re eager to help.

Our job is not to judge your decisions, it’s to help you get on the right path.

6. Create an estate plan to take care of your loved ones

A surprisingly large number of people think that a will is “just for old people.” In fact, as of 2025, only 24% of people have a will in place, most of them are 65 and older. And among those who do have wills, more than half have not updated their will in the last five years.

An updated will is an essential piece of taking care of your loved ones, no matter how old you are. Whether it’s having more kids, providing for grandchildren, or getting divorced, your will should reflect your life and represent the legacy you want to leave.

Any good financial advisor will ensure that you have a will set up and it is frequently updated to match your life circumstances.

Financial advisors often act as a “quarterback” for people who want to leave a legacy that will protect and provide for their family. We coordinate with estate planning attorneys and other professionals to ensure that your plan is set up exactly how you want it.

7. Align your money with your values

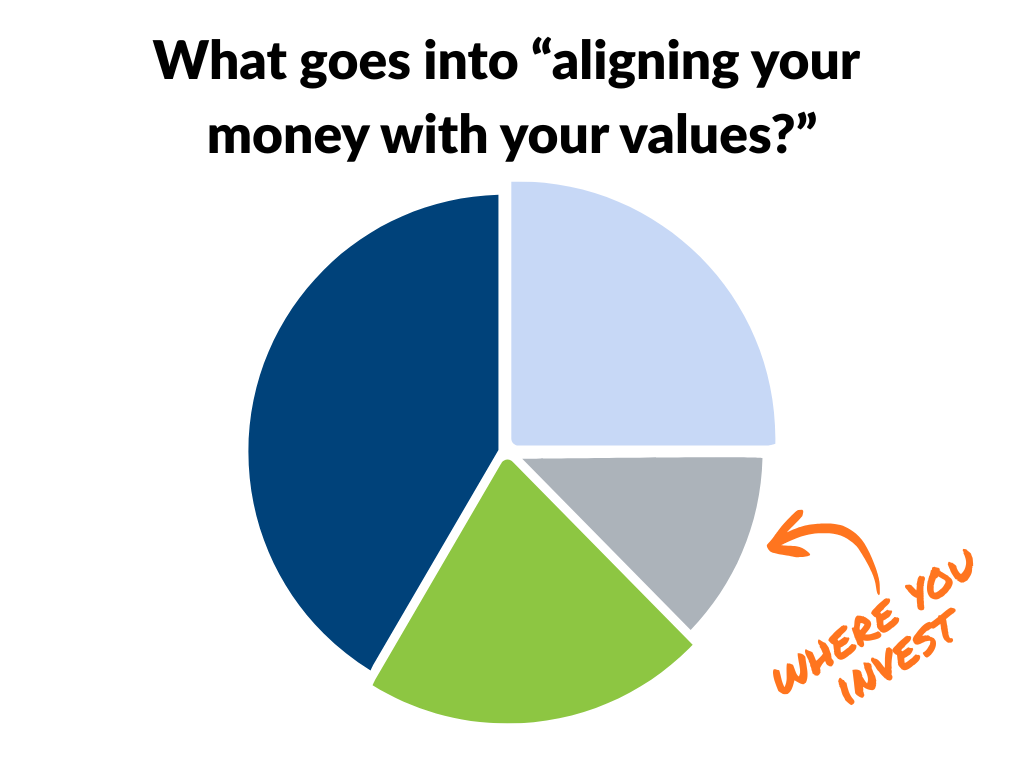

What does it mean to align your money with your values? Most people think it means investing in companies that align with your political or religious beliefs. But if values-based financial planning were a pie chart, “where you invest” would be one of the smallest slices for most people.

When we talk about aligning your money with your values, we mean saving and spending your money on the things that matter most to you, whether that’s time with family, traveling, experiences, staying healthy, etc. Investing is part of the plan, but primarily in how it can serve your ideal lifestyle.

According to a recent study, the top three values people cited as most important to them were family, health/well-being, and financial stability. Unfortunately, that same study said that 71% of Americans say their financial decisions rarely or only sometimes align with their values.

That’s our first step at Clarity: To understand the values that drive you so we can help you build a financial plan that serves the life you want to live.

8. Stay on top of how the latest legislation changes affect your plan

If you thought choosing stocks was complicated, try navigating the ever-changing tax laws. Some estimates say that, on average, one change is made to the U.S. tax code every day.

Just this year, the One Big Beautiful Bill Act changed and introduced several tax codes, such as:

- Lower tax rates for seniors

- Increased SALT deductions

- Increased estate tax exemption

You may be thinking, “I have an accountant who takes care of tax stuff, why would I need a financial advisor?”

You’re right, tax legislation is primarily relevant to accountants.

But the lower tax rate for seniors is intended to act as a kind of tax “exemption” for people receiving Social Security, which means you get to keep more of your Social Security income, which could mean several things, for instance:

- More money from Social Security could mean that you don’t need to use as much of your required minimum distributions (RMDs) each year, which could free up a good amount of spending money, which could make that trip you’ve been saving up for only two years away rather than three. Or you could help your grandson pay his college tuition. Or you could use it to help your daughter put a down payment on a new house.

Your accountant will make sure you get the new tax exemption, and they may even tell you to adjust your IRA distributions accordingly. But they don’t understand your values, your goals, and your larger financial plan well enough to help you decide what to do with the money, and how to best move the money around to avoid penalties.

An accountant looks backward at what happened last year. A financial advisor looks forward to what’s coming up and helps you make an informed decision.

Which path will you choose?

If you decide to work with an advisor, we hope you’ll consider reaching out to us. The best way to do that is to fill out our Get Started form here. Or, if you prefer, you can call our office at 541-753-1898.

At Clarity Wealth Development, we work with people who have worked hard to save for their future, and would rather talk about life than money. If that sounds like you, then we hope to hear from you soon!